If you need a straightforward US mileage guide for 2026, start here. Whether you are trying to get reimbursed by an employer or preparing a self-employed deduction, the first job is sorting the trip, the rule set, and the record.

The current federal rates come from the IRS 2026 mileage rate announcement and the recordkeeping rules live in Publication 463. If you want a mileage tracker app handling the log while you work, MyCarTracks automatic mileage tracking can capture trips before reimbursement, payroll, or tax questions pile up.

This article is educational and is not tax, legal, payroll, employment, or financial advice. Mileage rules change by federal tax treatment, state law, employer policy, vehicle program, and tax year. Check the official source and a qualified professional before relying on a calculation.

Quick answer

Start by identifying whether the trip is for employee reimbursement, a self-employed deduction, or a company vehicle program. For 2026, the IRS business standard mileage rate is 72.5 cents per mile, but the rate only helps after you confirm the trip qualifies and keep mileage tracking records with the date, destination, purpose, and miles.

Who this guide helps and where to start

If you already know the question you need to answer, jump straight to the deeper article:

- Current IRS Mileage Rates for 2026

- Historical IRS Mileage Rates by Year

- What Is Mileage Reimbursement?

- IRS Mileage Log Requirements

- How to Claim Mileage on Taxes

- Car Allowance vs Mileage Reimbursement

If you want the broader product overview after you pick the right workflow, MyCarTracks explains the app and team features behind the recordkeeping side.

Core mileage tracking basics

Mileage reimbursement is the payment you may receive when you use a personal vehicle for work. In most US workflows, it covers business use of a car, van, pickup, or panel truck and is calculated either with a per-mile rate or a formal vehicle program. It is meant to address vehicle costs tied to business driving, not ordinary commuting or personal trips.

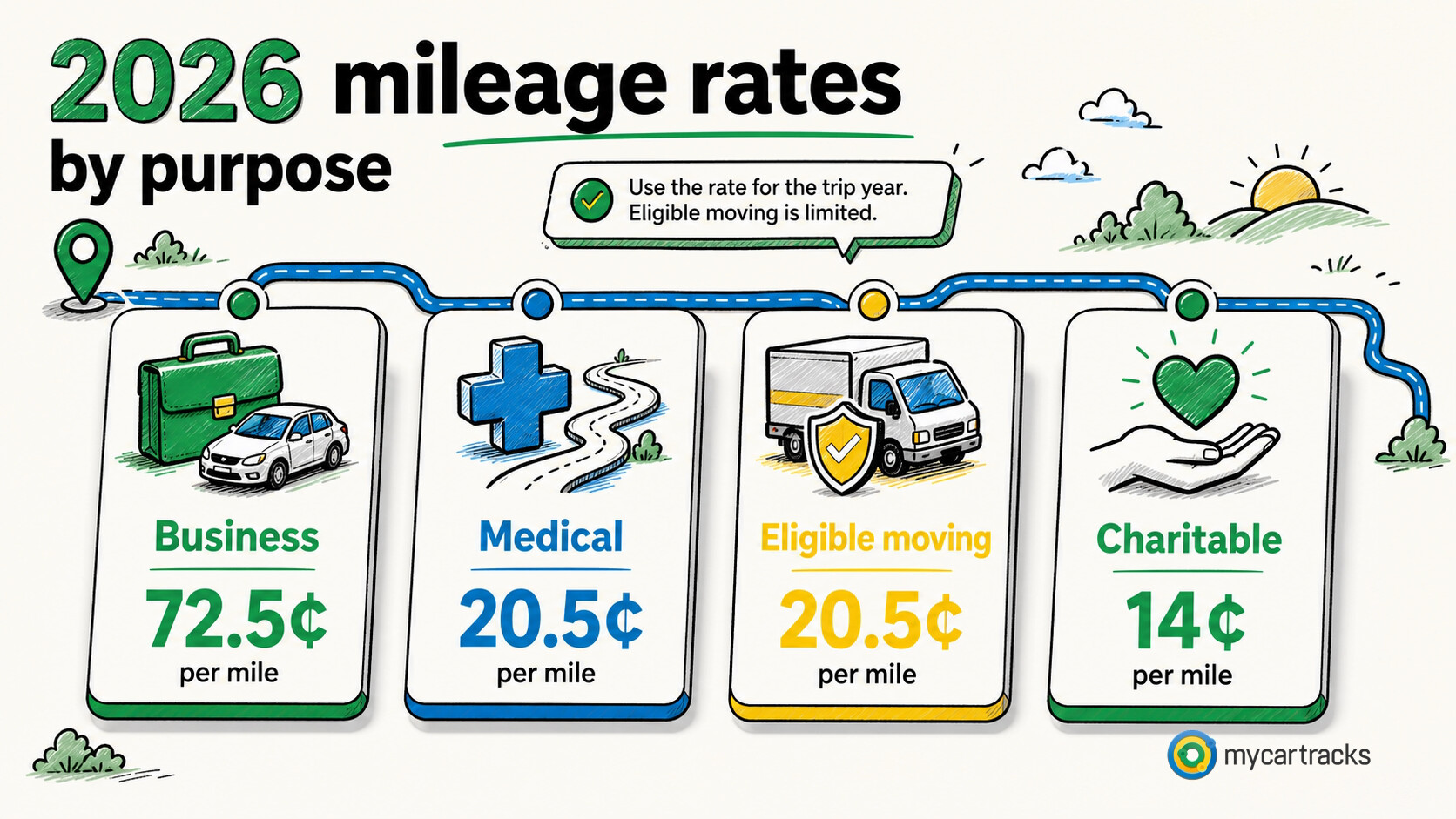

Current federal mileage rates

For 2026, the IRS standard mileage rates and the year-end rate announcement give you the current federal starting point:

| Use | 2026 rate |

|---|---|

| Business | 72.5 cents per mile |

| Medical | 20.5 cents per mile |

| Moving for eligible active-duty Armed Forces members and certain intelligence community members | 20.5 cents per mile |

| Charitable service | 14 cents per mile |

Those rates apply to gasoline, diesel, hybrid, and fully electric automobiles covered by the standard mileage method. If you need the year-by-year table or a closer comparison with 2025, use Current IRS Mileage Rates for 2026 and Historical IRS Mileage Rates by Year.

Which trips usually count as business travel

Business mileage is usually about travel between work locations, not travel between home and your regular workplace. Common examples include:

- traveling from your main work location to a temporary work location

- going from your main job to a second job on the same day

- moving between a temporary work location and a second job

- driving from home to a temporary work location when your regular work location is elsewhere

Trips that usually do not qualify include:

- driving from home to your regular workplace

- driving from home to a second job

Regular workplaces, temporary assignments, and second jobs are not treated the same. If the trip purpose is unclear, do not assume the rate alone will fix the classification problem.

Examples of trips people usually submit

Typical reimbursable or deductible trips include driving from one office to another, going from the office to a client site, making a work errand to a supply store or post office, or traveling to a short-term assignment away from the regular work location. Parking and tolls may need to be tracked separately instead of being buried inside the mileage line.

When home-based work changes the analysis

If your home qualifies as your main place of business, travel from home to another work location for the same business may be treated differently from an ordinary commute. That is one reason Publication 463 and the filing workflow behind Schedule C matter for self-employed readers. If this is your situation, go deeper with Self-Employed Mileage Deduction Rules.

When reimbursement becomes taxable

Mileage reimbursement is often non-taxable when it is tied to business driving, documented in a reasonable time, and handled under a substantiated reimbursement arrangement. Amounts paid above the supported rate or paid without adequate records can be treated differently for payroll and income reporting under the reimbursement rules in Publication 463. For the deeper breakdown, use Is Mileage Reimbursement Taxable Income?.

Rules for employees

Employees should start with the employer policy, not with a tax shortcut. A clean claim needs the trip date, destination, business purpose, miles, and any separately handled parking or tolls. Employees also need to know that federal reimbursement customs and state expense rules are not the same thing. If you work in California, Illinois, or Massachusetts, move to the state-specific article before relying on a quick answer. Federal deduction treatment is also narrower than many workers expect, as explained in Publication 463.

Rules for self-employed taxpayers

Self-employed readers usually care about two things: whether the trip is actually business driving and whether the standard mileage method or actual expenses fits the vehicle better. Publication 463 explains both methods, and Schedule C is where many sole proprietors report the result.

If the vehicle is used only for business, you may be looking at the full set of allowable vehicle costs. If it is mixed-use, only the business portion belongs in the deduction file. Use How to Claim Mileage on Taxes, Standard Mileage Rate vs Actual Expenses, and Self-Employed Mileage Deduction Rules when you need the filing and method side next.

Rules for employers

Employers usually choose between the standard mileage rate, FAVR, a car allowance, or a company-car or fleet approach. The right method depends on driving patterns, payroll treatment, administrative capacity, and the level of control the company needs.

At the federal level, the IRS rate is a tax and substantiation benchmark, not a rule that forces every employer to use that exact number. Companies may choose a higher or lower rate, but unsupported excess amounts and weak records can create tax and payroll problems. If you reimburse employees directly, the core compliance questions still come back to business connection, timely substantiation, and how excess payments are handled under Publication 463.

Leaving employees without a defined program usually creates the most disputes because the trip record exists but nobody agrees how it should be paid. For implementation details, continue with Mileage Reimbursement Rules for Employers, How to Create a Mileage Reimbursement Policy, FAVR Reimbursement Plans Explained, and Car Allowance vs Mileage Reimbursement.

Keep mileage tracking records that hold up later

The strongest mileage logs are created at or near the time of the trip, which is the recordkeeping standard explained in Publication 463. At minimum, capture the date, destination or route, business purpose, miles driven, and the vehicle used. Mixed-use vehicles also need total annual miles.

If you want the export side to stay organized for tax returns, manager approvals, or year-end review, MyCarTracks business mileage reports can keep the mileage logs grouped by driver, vehicle, pay period, or tax year while the trip details are still easy to explain.

How to calculate a mileage claim

The basic calculation is simple: reimbursement or deduction amount = approved business miles x the rate for that year and purpose. For example, 100 business miles x 72.5 cents gives you $72.50 for a 2026 business-rate calculation before separately handled parking or tolls. If you are testing actual expenses instead, divide business miles by total miles to get the business-use percentage and then apply that percentage to the supported vehicle costs. Split reports that cross tax years so 2025 miles do not get priced with 2026 rates.

Decision workflow

Use the same decision path before applying a rate or submitting a report:

- Identify the person or entity using the record: employee, employer, self-employed worker, volunteer, contractor, owner, or fleet manager.

- Identify the purpose: reimbursement, deduction, payroll support, job costing, customer billing, vehicle program review, or fleet reporting.

- Identify the tax year and the US rule set that applies. Do not mix business, medical, moving, charitable, reimbursement, and state-law rules in one calculation.

- Confirm whether the trip qualifies under the relevant source. A route can be real and still be personal, commuting, or outside the policy.

- Apply the rate, method, or program only after the trip record is complete.

- Save the source, report, approval, and payment record together.

That order matters. Many mileage errors happen because someone starts with a rate and then tries to make the trip fit it. A stronger workflow starts with the trip facts and uses the rate only at the calculation step.

Category map

The Mileage Guides category should work like a practical library, not a pile of isolated posts. A reader who starts with current IRS rates should be able to move naturally into mileage logs, standard mileage versus actual expenses, employee reimbursement, and state rules. A reader who starts with car allowance questions should be able to move into FAVR, company cars, reimbursement policy, and fleet records.

The goal is to keep rates, reimbursement, deductions, mileage logs, and vehicle-program choices tied to the same trip record. When the record is clean, the later tax, payroll, and policy decisions become much easier to explain and defend.

Practical example

Suppose a field employee drives from home to a regular office, then to a client site, then to a supplier, and then home. The regular office commute may need to stay separate from the business legs. The client and supplier trips may qualify under the employer policy. Parking or tolls may be reimbursed separately. If the employee also stops for a personal errand, that segment should be split or noted.

Now suppose a self-employed consultant drives the same route. The record may be used for a tax deduction or business expense calculation instead of employee reimbursement. The consultant may need total annual vehicle distance, business distance, and receipts for actual expenses. The route is similar, but the workflow is different because the person using the record is different.

This is why mileage content should not stop at a formula. The article needs to explain the role, the trip purpose, the record, and the calculation method.

Record quality standard

A mileage record is stronger when it can answer a skeptical review without the driver being present. The reviewer should be able to see the trip date, route or destination, distance, purpose, vehicle, category, and supporting documents. If the record depends on a vague memory such as “probably a client visit,” it is weak. If it points to a calendar entry, job ticket, customer, delivery, work order, reimbursement request, or receipt, it is much easier to trust.

For teams, a second quality standard matters: the report should be consistent across drivers. If one employee submits odometer readings, another submits rounded estimates, and another submits only fuel receipts, approvals become subjective. A shared format protects employees and employers because everyone knows what proof is expected before money or tax treatment is involved.

Source handling

Save the official source used for each rate, rule, or policy decision. For public articles, that means linking to the IRS or the relevant state source rather than repeating unsupported third-party claims. For internal company use, it means saving the policy version and source rate that were active when the trip was paid. This matters when a reader later asks why a 2026 trip was calculated differently from a 2025 trip, or why one state required a different reimbursement workflow from another state.

Review checklist

- Is the trip business, commuting, personal, medical, charitable, or another category?

- Is the rate from the correct tax year and rule set?

- Are different trip categories kept separate?

- Does the record name the vehicle and driver?

- Does the business purpose make sense without extra memory?

- Are parking, tolls, and other route costs handled separately?

- Are total annual vehicle miles needed?

- Is the reimbursement policy saved with the report?

- Are state-specific rules relevant?

- Is a professional review needed before filing, payroll, or policy decisions?

Operational notes

The cleanest mileage programs use a short feedback loop. Drivers review trips weekly. Managers approve or reject claims on a predictable schedule. Finance exports reports before closing the period. Policy owners review official rate changes at least annually. When each role owns a small part of the workflow, mileage records stay useful instead of becoming a year-end cleanup project.

The workflow should also have an exception lane. A missed trip, lost receipt, changed vehicle, late submission, temporary assignment, or unusual route should not be hidden in the normal report. Mark it, explain it, approve it separately, and keep the note with the record. Exceptions are normal; undocumented exceptions are what create risk.

For public-facing content, this operational layer is what raises the article above a definition page. Readers should leave knowing not only what the rule or rate is, but how to collect records, review them, correct problems, and produce a report that someone else can trust.

When to get professional review

Get tax, payroll, legal, or accounting review when the answer affects a filed return, employee wages, worker classification, taxable benefits, multi-state reimbursement, FAVR design, or a dispute over unpaid expenses. A mileage app can make the record cleaner, but it cannot decide the legal or tax treatment by itself.

Records to keep

Keep these records before a deadline or tax return forces the issue:

- date of each trip

- start and end location, destination, route, or client/job context

- business purpose

- distance driven

- vehicle used

- driver or employee name when a team is involved

- total odometer readings where required

- receipts for fuel, charging, repairs, parking, tolls, insurance, registration, and other vehicle costs

- reimbursement requests, approvals, denials, and employer policy documents

- tax-year rate source used for each calculation

Common mistakes

- using the current rate for an older tax year

- mixing commuting, personal errands, and business miles

- saving only payout, calendar, or bank records without a mileage log

- forgetting total annual miles when actual expenses or business-use percentages matter

- treating an employer reimbursement policy as if it were a tax rule

- treating a tax rule as if it were an employer reimbursement promise

- missing parking, tolls, support trips, return trips, and supply runs

- waiting until tax season to explain routes from memory

FAQ

Does mileage reimbursement already include gas?

Usually, yes when the standard mileage method is being used. The per-mile rate is designed to represent the operating cost of the vehicle, so do not layer fuel on top of the same miles without checking the method first.

Can you claim tolls and parking separately?

Often, yes for qualifying business travel when those costs are supported. They should stay separate from the mileage line so the record shows exactly what was reimbursed or deducted.

Should an employer always use the IRS mileage rate?

Not always. Many employers use it because it is familiar and easy to explain, but a company may choose a higher or lower rate or a different program structure. What matters is that the policy is clear, the records are clean, and any tax treatment questions are handled correctly.

Do electric vehicles use a different IRS mileage rate?

No separate business rate applies just because the vehicle is electric. The current IRS rate announcement uses the same mileage rate framework for gasoline, diesel, hybrid, and fully electric automobiles covered by the standard mileage method.

MyCarTracks workflow

Use MyCarTracks as the trip record layer, then let the tax, payroll, or accounting workflow decide how the records are used.

- Record trips automatically.

- Classify business and personal driving while the trip is still fresh.

- Add tags for employee, vehicle, client, project, platform, or state.

- Review mileage weekly so personal stops and unclear routes are fixed early.

- Export reports by tax year, pay period, vehicle, driver, or reimbursement cycle.

What to read next

- Current IRS Mileage Rates for 2026

- Historical IRS Mileage Rates by Year

- What Is Mileage Reimbursement?

- IRS Mileage Log Requirements

- How to Claim Mileage on Taxes

- Car Allowance vs Mileage Reimbursement