Mileage tracking helps you understand whether a FAVR reimbursement plan is worth the added complexity. A fixed and variable rate program is usually worth considering when one national cents-per-mile rate no longer matches how your employees actually drive, where they drive, or what it costs them to keep a work-ready vehicle.

That is the problem FAVR is designed to solve. A fixed and variable rate plan combines a fixed payment for ownership-style costs with a variable payment for mileage-based operating costs. The IRS framework for that structure lives in section 6 of Revenue Procedure 2019-46, and the 2026 maximum standard automobile cost for a FAVR plan is $61,700 under Notice 2026-10.

If your first problem is getting the mileage record right before you model the reimbursement, MyCarTracks automatic mileage tracking can help you capture trips, business purpose, and review periods before the program math starts.

This article is educational and is not tax, legal, payroll, employment, or insurance advice. FAVR is a formal reimbursement method with eligibility, vehicle, and recordkeeping rules that should be reviewed against the current tax year and the company’s policy design before launch.

Quick answer

FAVR stands for fixed and variable rate. It reimburses business driving in a personal vehicle through a fixed payment for ownership costs and a mileage-based payment for operating costs. It can be more precise than a flat allowance or a single national mileage rate, but it only works well when the company can support the IRS rules, the recordkeeping, and the ongoing updates.

What is FAVR?

FAVR is a reimbursement method for employees who use personal vehicles for work. Instead of treating every cost as if it rose evenly with each mile, it separates the costs of simply keeping a work-ready vehicle from the costs that move with business driving.

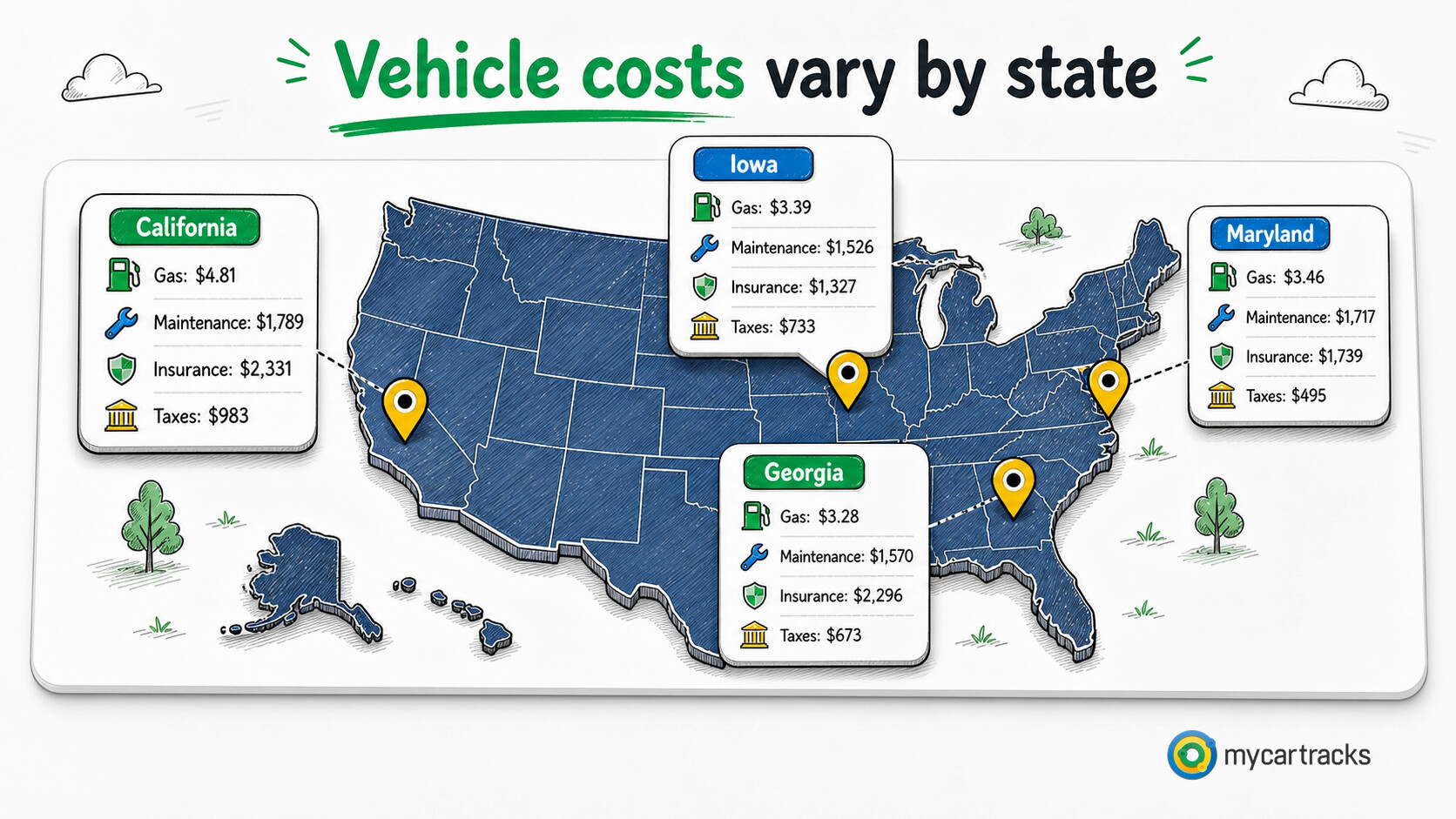

That matters because insurance, registration, and depreciation do not behave the same way as fuel, tires, and routine maintenance. A driver can have a slow month and still carry real ownership costs. A driver in a higher-cost area can also face a very different expense profile from someone performing the same job in a lower-cost area.

When a FAVR plan satisfies the IRS requirements, the business can use that structure as part of an accountable reimbursement arrangement. It is not “tax-free because it is called FAVR.” It is only handled that way when the plan and the records actually meet the rules.

What are the benefits of a FAVR car allowance vs. other vehicle programs?

FAVR stays popular because it solves several problems at once when a workforce has enough regular business driving to justify the setup.

Fairness

FAVR is often the fairest option when employees drive different distances or live in different cost areas. A flat allowance can ignore those differences, and a single national mileage rate can still miss how ownership costs behave.

By splitting fixed and variable costs, a FAVR plan can handle a slow month differently from a heavy month.

Cost accuracy

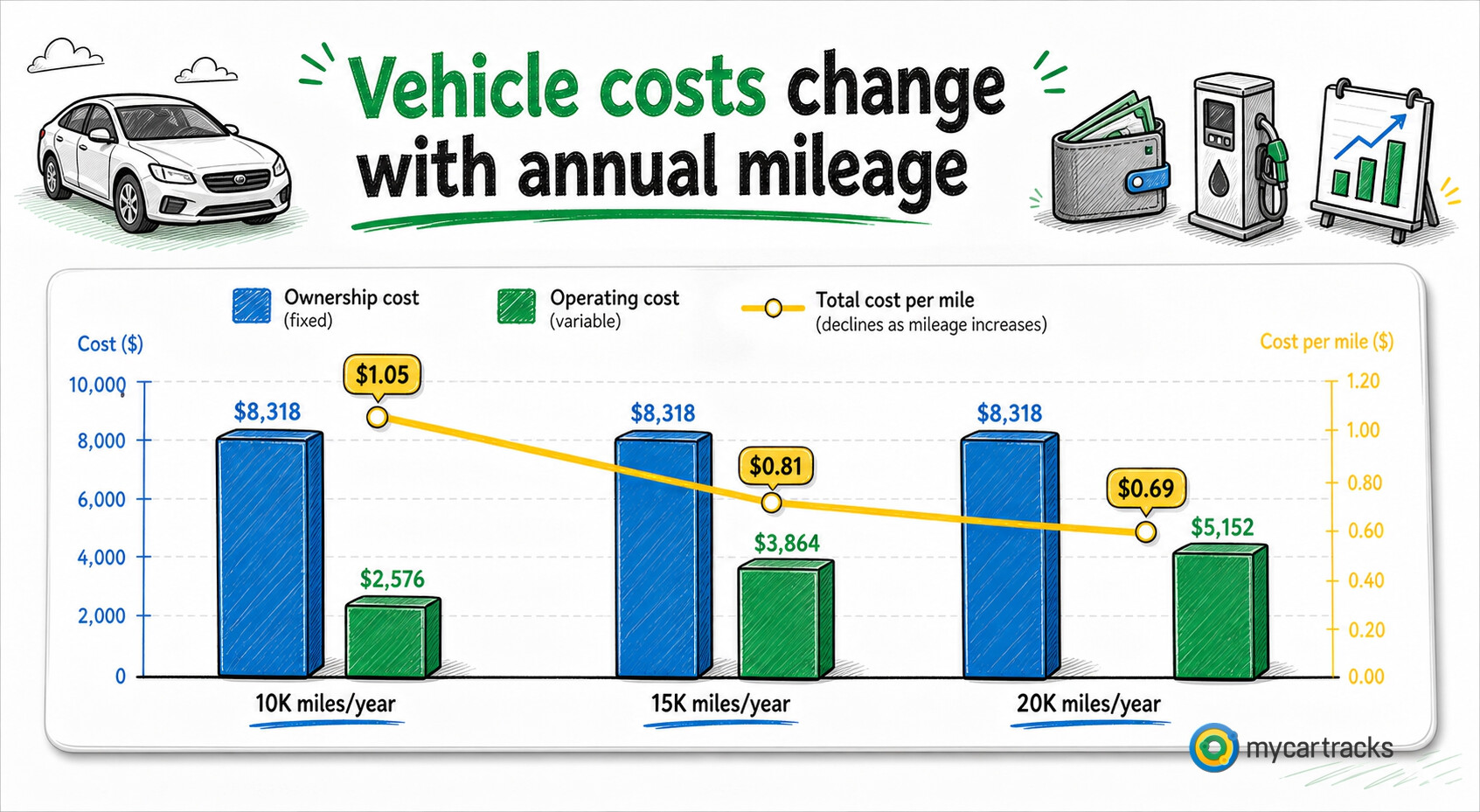

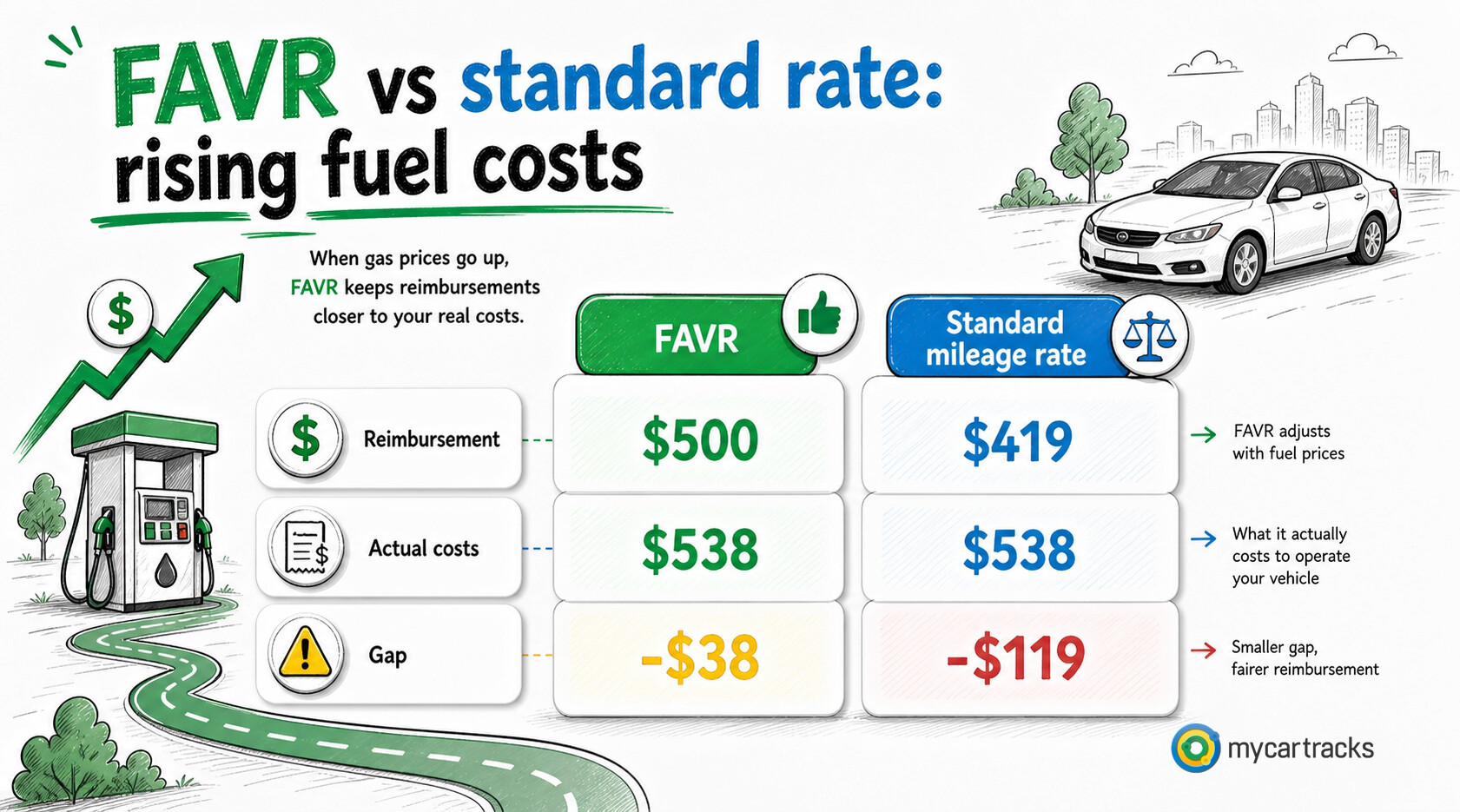

FAVR can also be more accurate for the business. A cents-per-mile program increases in a straight line with every mile, even though an employee’s real cost per mile can change as fixed ownership costs are spread across more or fewer miles.

That can reduce overpayment in some roles while still covering the vehicle burden more realistically than a flat stipend.

Predictability

FAVR is more adaptable than a flat allowance. The fixed part gives employees and finance a steadier baseline than a single cents-per-mile program, while the variable side still moves with driving and local operating costs.

Flexibility and alignment to objectives

Within the IRS rules, businesses still have real design choices. A company picks the standard automobile, retention period, insurance assumptions, and overall reimbursement structure.

That flexibility is useful when leadership has a target budget or different employee groups with different vehicle expectations.

Risk management

FAVR programs often push companies to define vehicle standards, insurance requirements, and employee reporting responsibilities more clearly than a casual stipend would.

It also makes it easier to combine mileage tracking, insurance checks, and policy enforcement in one process.

Tax efficiency

When a FAVR plan satisfies the IRS rules and is run as part of an accountable arrangement, it can be much more tax-efficient than a simple taxable allowance.

A basic cents-per-mile reimbursement can provide the same kind of accountable-plan treatment, but FAVR gives the business more room to reflect ownership costs and local variation.

Is FAVR right for your business?

FAVR is a strong fit for some businesses and the wrong amount of complexity for others.

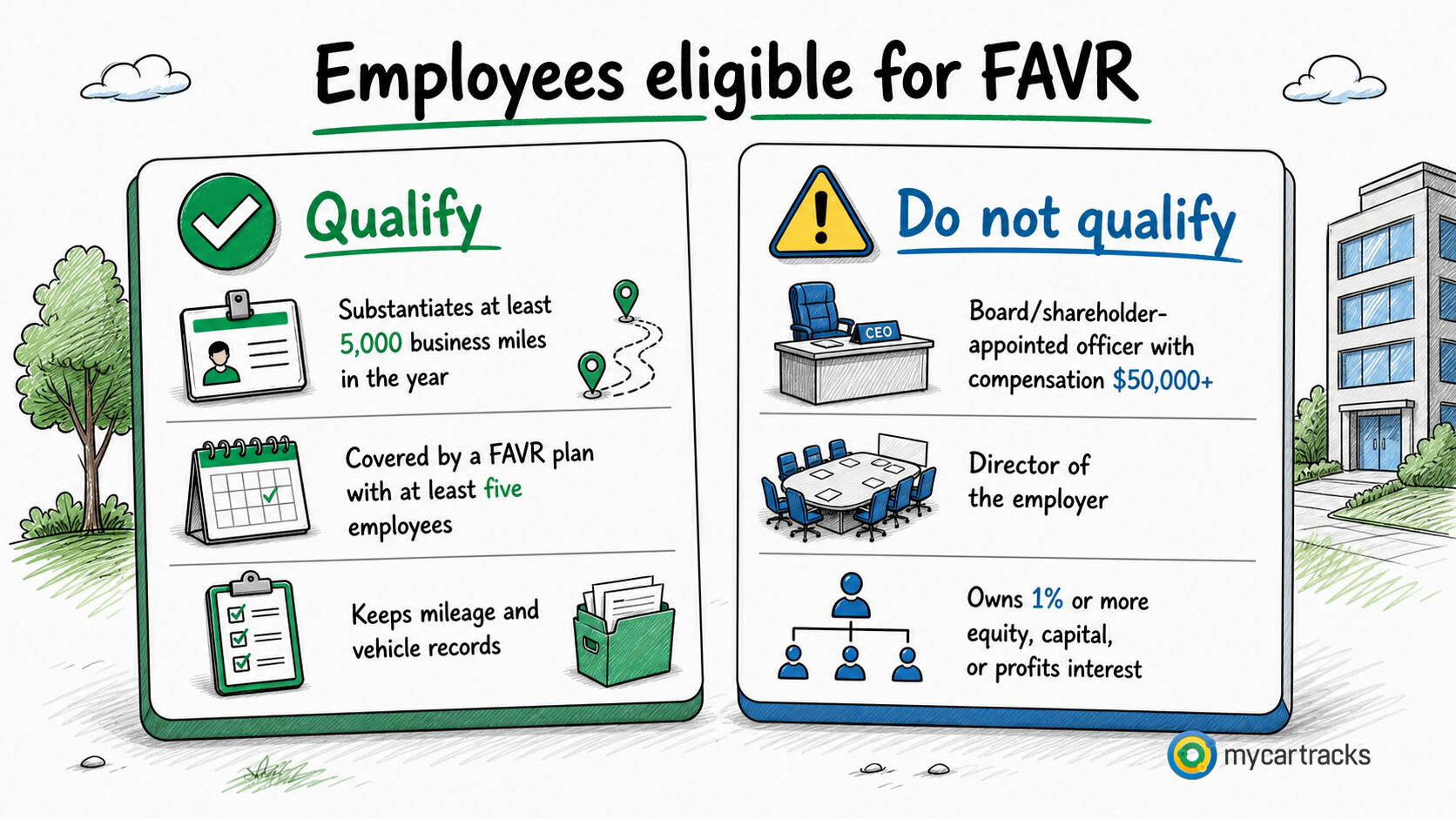

At a minimum, the IRS structure is not built for one or two occasional drivers. Revenue Procedure 2019-46 says a payor may not provide a FAVR allowance unless FAVR allowances cover at least five employees at all times during the calendar year, and it may only cover an employee who substantiates at least 5,000 business miles for the year or, if greater, 80 percent of the annual business mileage used in that FAVR plan.

Beyond those baseline requirements, FAVR tends to fit best when the company has:

- employees spread across different cost areas

- regular business driving that is too uneven for one flat rate

- several roles with different vehicle expectations

- a real need for cleaner spend control than a taxable car allowance can provide

- enough administrative discipline to maintain plan assumptions and records

If the workforce is tiny, mileage is occasional, or the company cannot keep clean trip and employee records, a simpler mileage reimbursement policy is often the better answer.

Market factors

Market conditions can make FAVR more attractive even if a company has been comfortable with a different program for years. Large fuel swings, expansion into higher-cost states, and wider differences between territories all make one national number feel rougher over time.

Hiring pressure can matter too. When employees are expected to show up with a work-ready vehicle but the reimbursement no longer feels connected to what that vehicle costs them, transportation policy becomes a retention problem rather than an accounting detail.

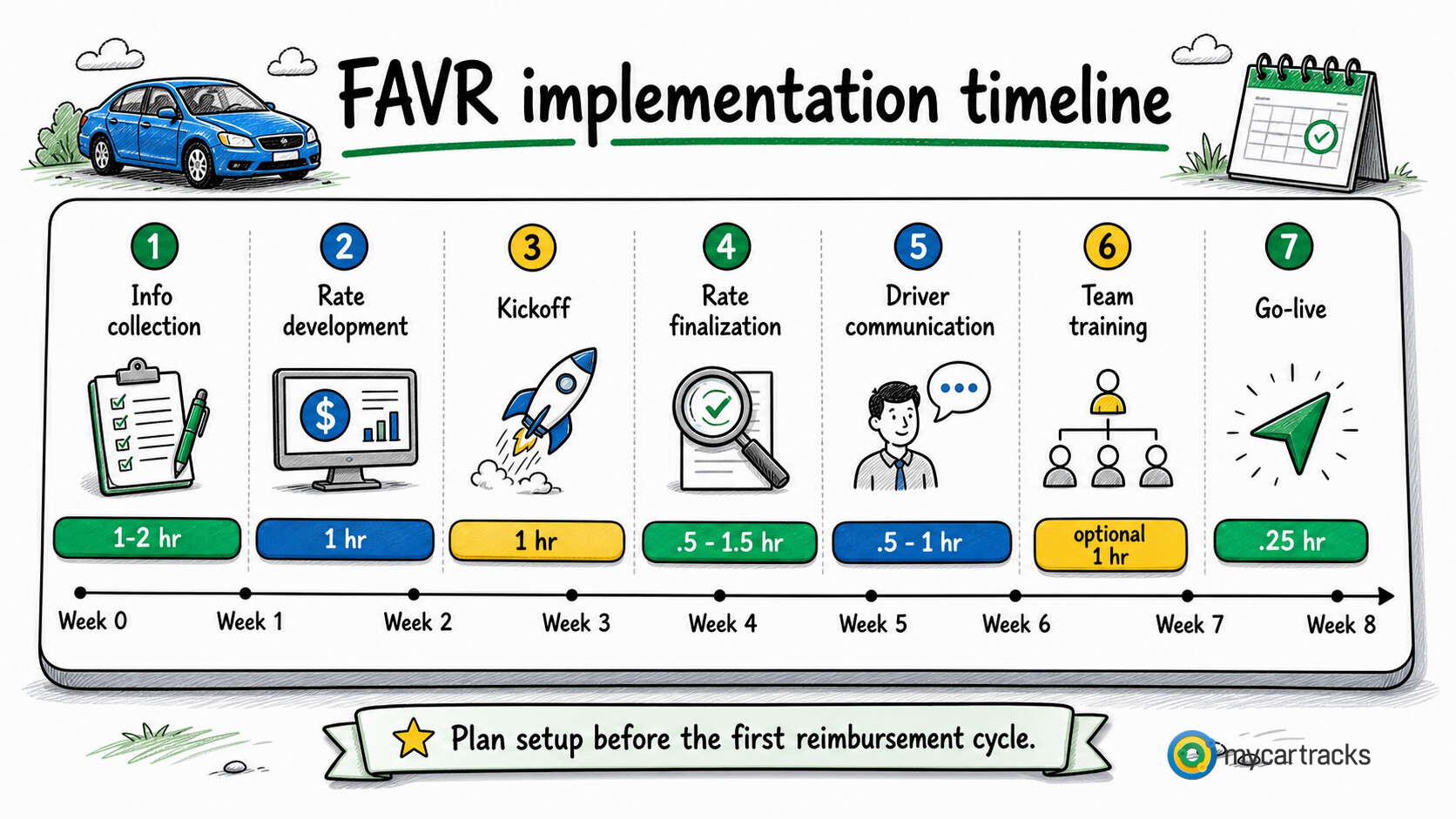

Policy design

FAVR policy design should be written down before the first reimbursement cycle. The company should define the covered roles, the standard automobile, the retention period, the insurance requirements, the mileage-proof standard, and what happens when an employee changes vehicles, territories, or mileage bands.

If those rules stay informal, the company usually ends up with a FAVR calculation model on paper and an allowance program in practice.

IRS FAVR guidelines in 2026

The IRS rules are the part that separates a real FAVR plan from a custom allowance that happens to use the acronym. The key 2026 points come from Revenue Procedure 2019-46 plus Notice 2026-10.

At a high level:

- FAVR allowances must cover at least five employees at all times during the year.

- A majority of covered employees cannot be management employees.

- An employee generally must substantiate at least 5,000 business miles for the year or, if greater, 80 percent of the plan’s annual business mileage.

- The annual business mileage used in the plan cannot be less than 6,250 miles for a calendar year.

- The plan’s standard automobile cost cannot exceed $61,700 for 2026.

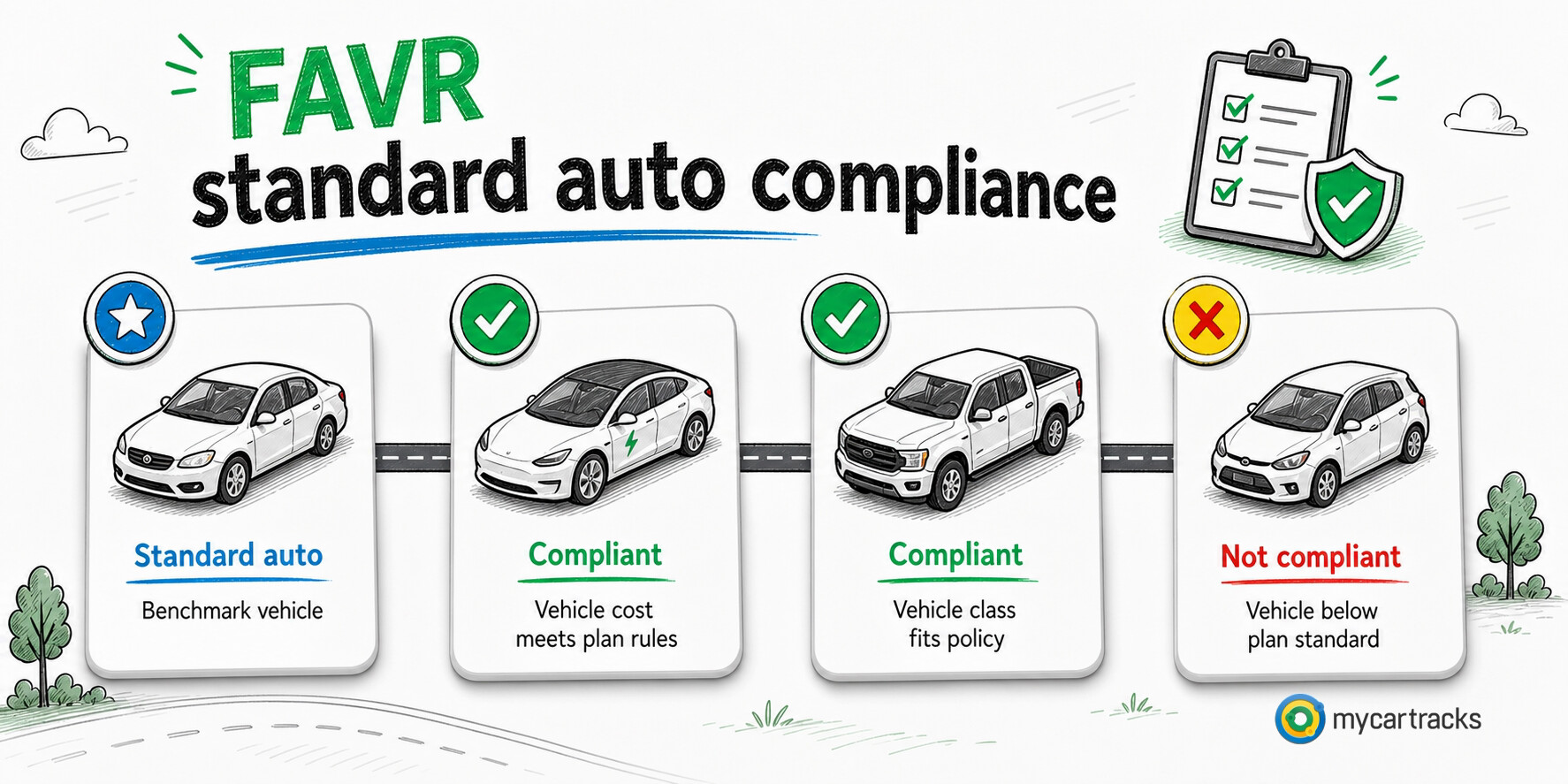

The employee’s vehicle must also fit the program. Revenue Procedure 2019-46 says the employee must own or lease the vehicle, the vehicle’s cost when new must have been at least 90 percent of the standard automobile cost used for the plan when the employee first receives the allowance for that vehicle, and the model year must stay within the program’s retention period.

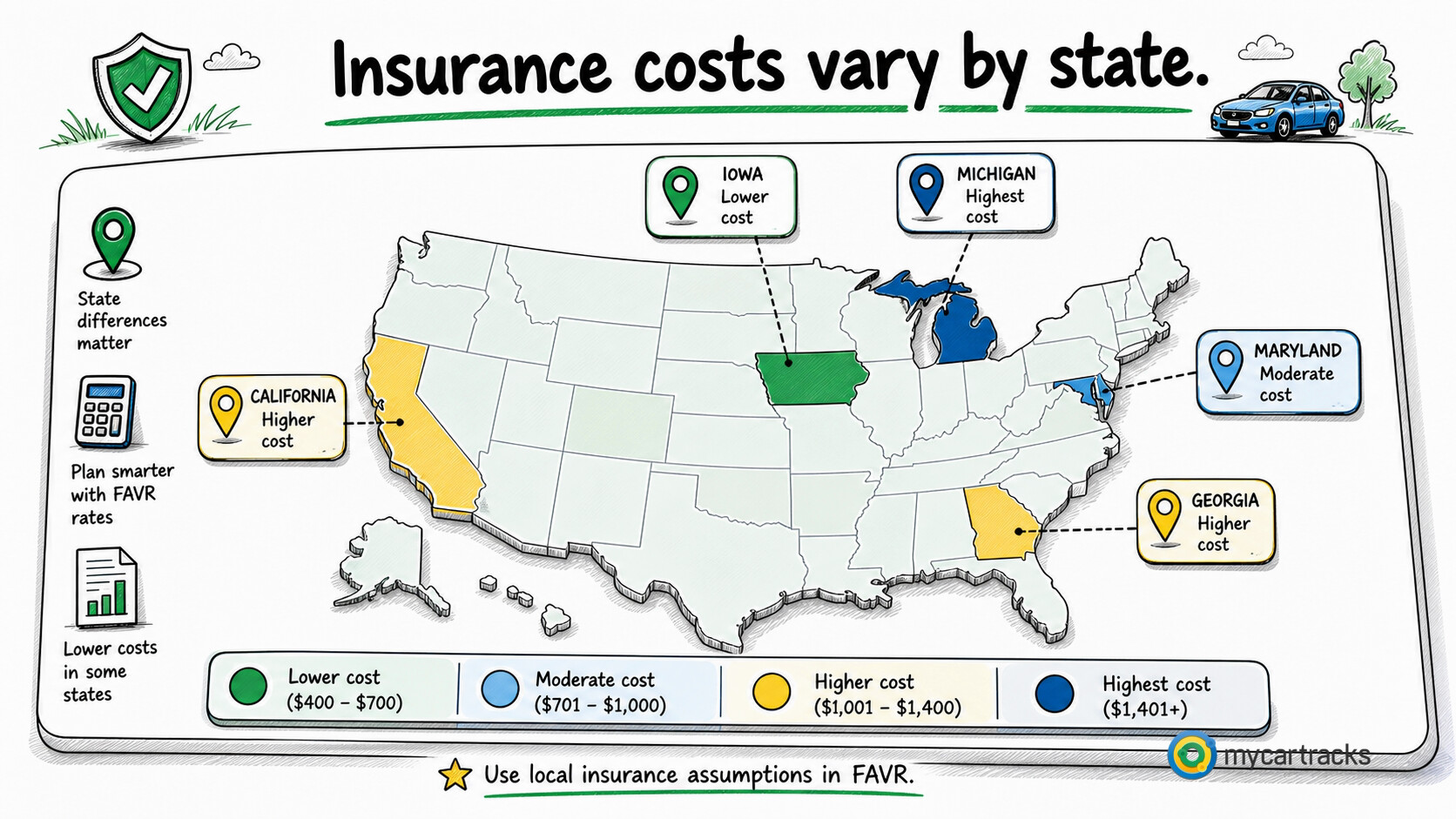

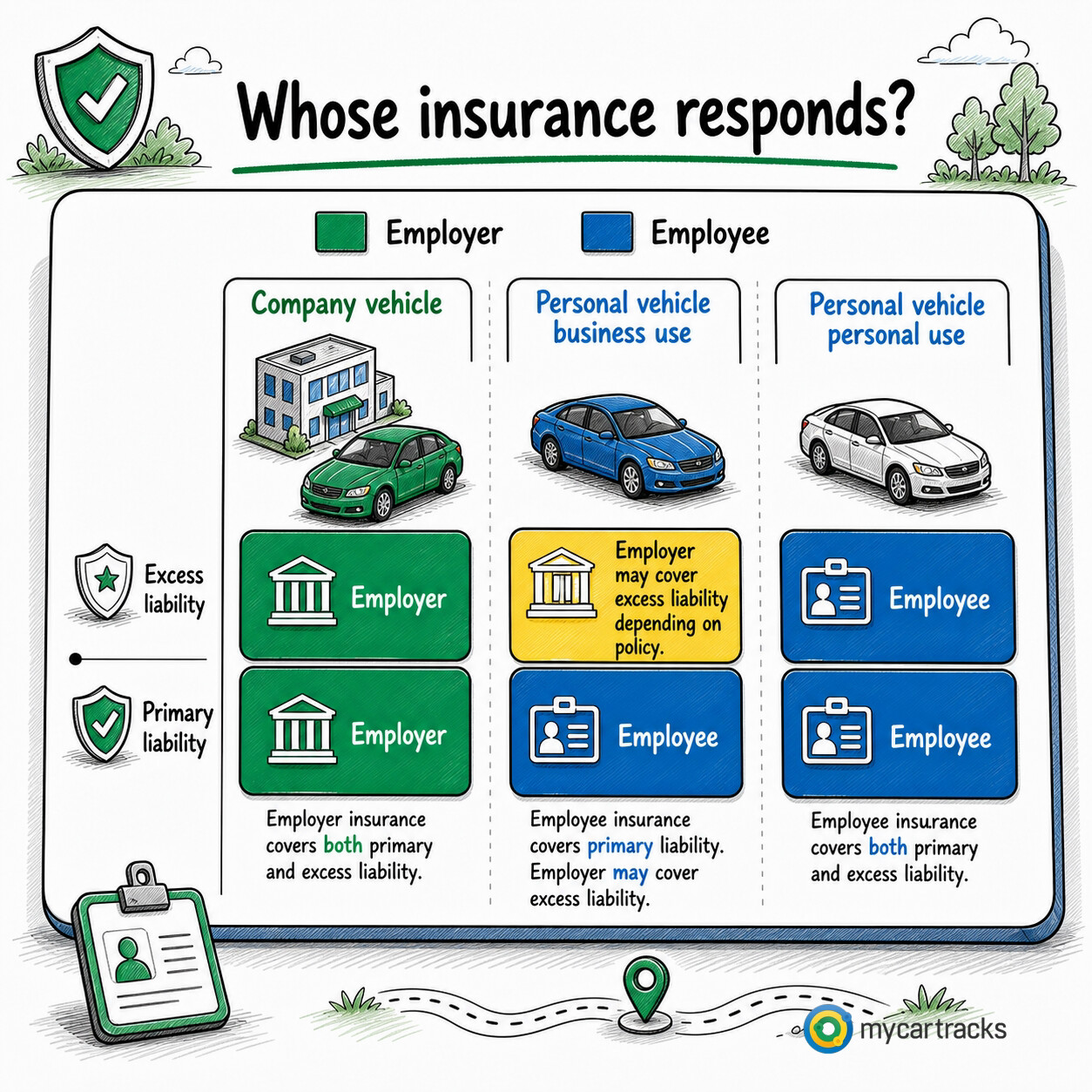

Insurance matters too. The plan’s insurance cost assumptions must be based on the rates charged in the employee’s base locality for the standard automobile, and the employee’s own coverage limits must be at least equal to the limits used in the program.

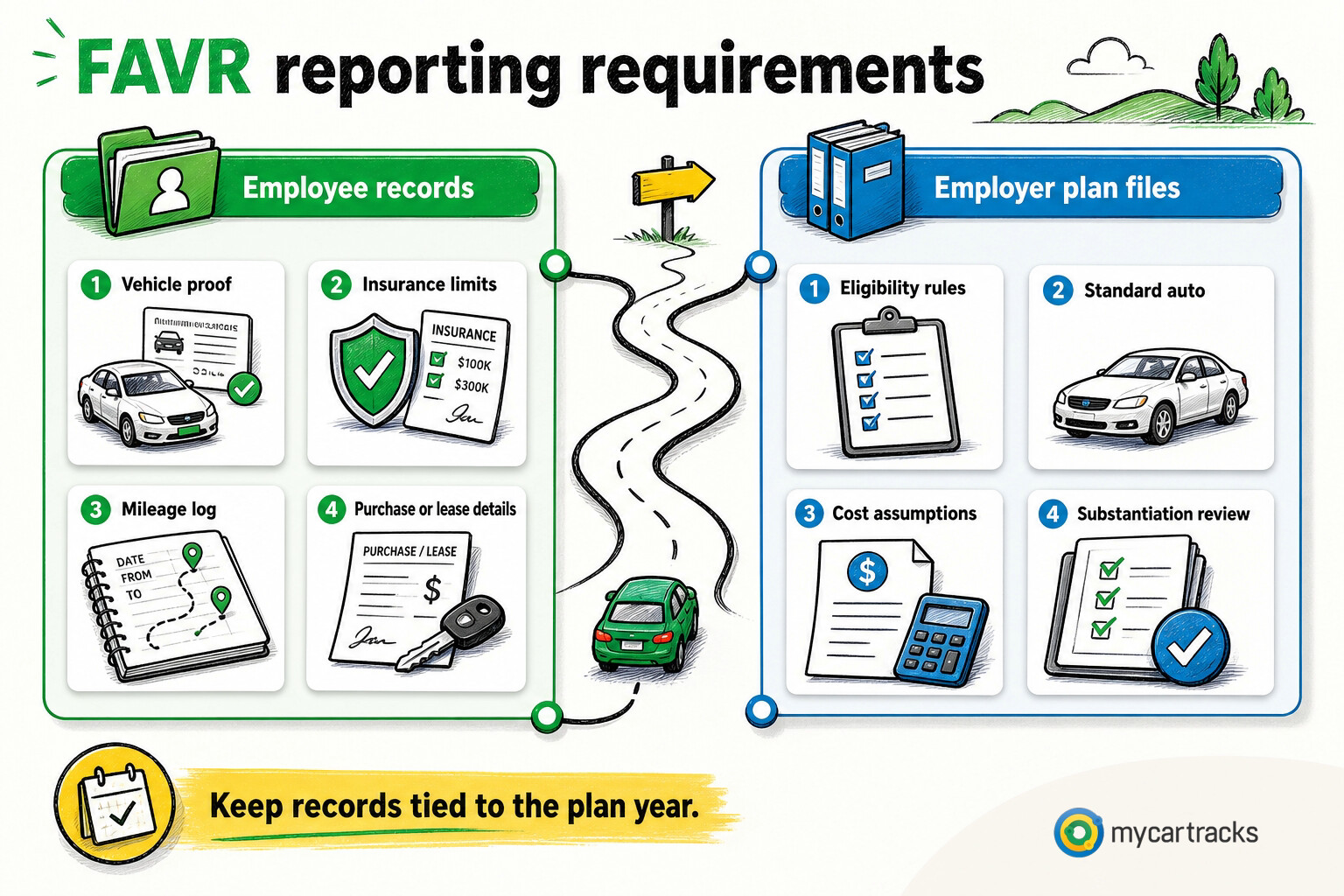

The reporting side is just as important. Employees must provide vehicle, insurance, price, and odometer information within 30 days after the plan first covers the vehicle, and certain items must be refreshed at the start of each calendar year.

Mileage tracking and recordkeeping

FAVR does not replace mileage tracking. It depends on it.

Employees still need a business-mileage record that shows the trip date, destination, business purpose, and miles driven. Without that file, the variable side cannot be supported properly and the accountable-plan treatment becomes much harder to defend.

The employer or its agent must also keep written records of the cost data, program assumptions, and employee information used to support the plan. IRS Mileage Log Requirements and What Is a Mileage Log? cover the proof standard in more detail.

How to calculate a FAVR allowance

FAVR is not one formula pasted onto every employee. It is a plan design process built from employee, vehicle, and cost assumptions.

1. Gather employee data

Start with the employee details that drive the model: home location, expected business mileage, and the employee group the person belongs to if the company runs more than one FAVR program.

The goal is to choose assumptions the company can explain and defend later.

2. Select a standard auto and retention period

Each FAVR program is built around a standard automobile rather than each employee’s exact car. The company picks the vehicle class and retention period, then applies the plan consistently to the covered employees.

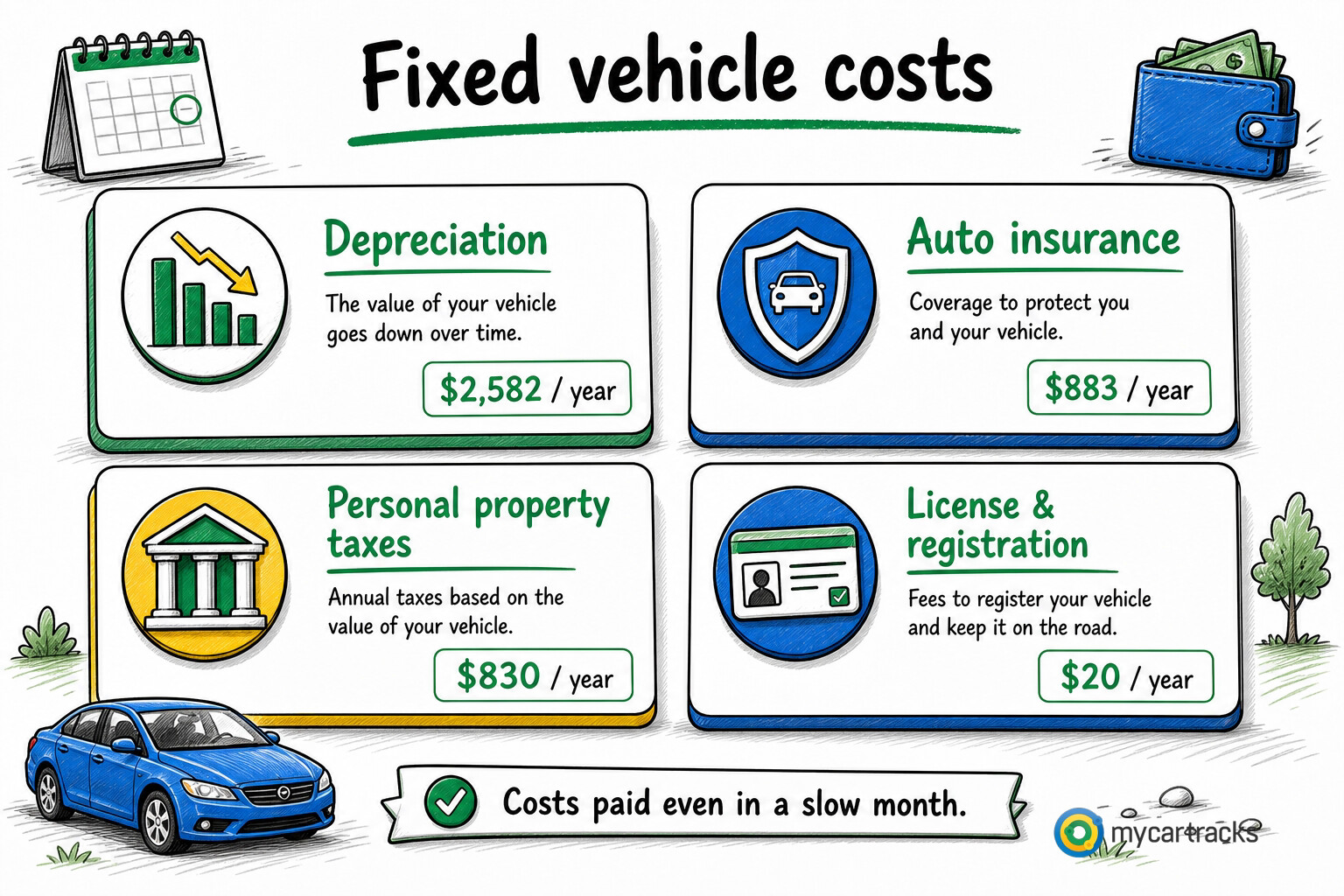

3. Set fixed rates

The fixed rate captures ownership-style costs such as depreciation, registration, taxes, and insurance. Those costs are usually annualized and turned into the pay-period amount.

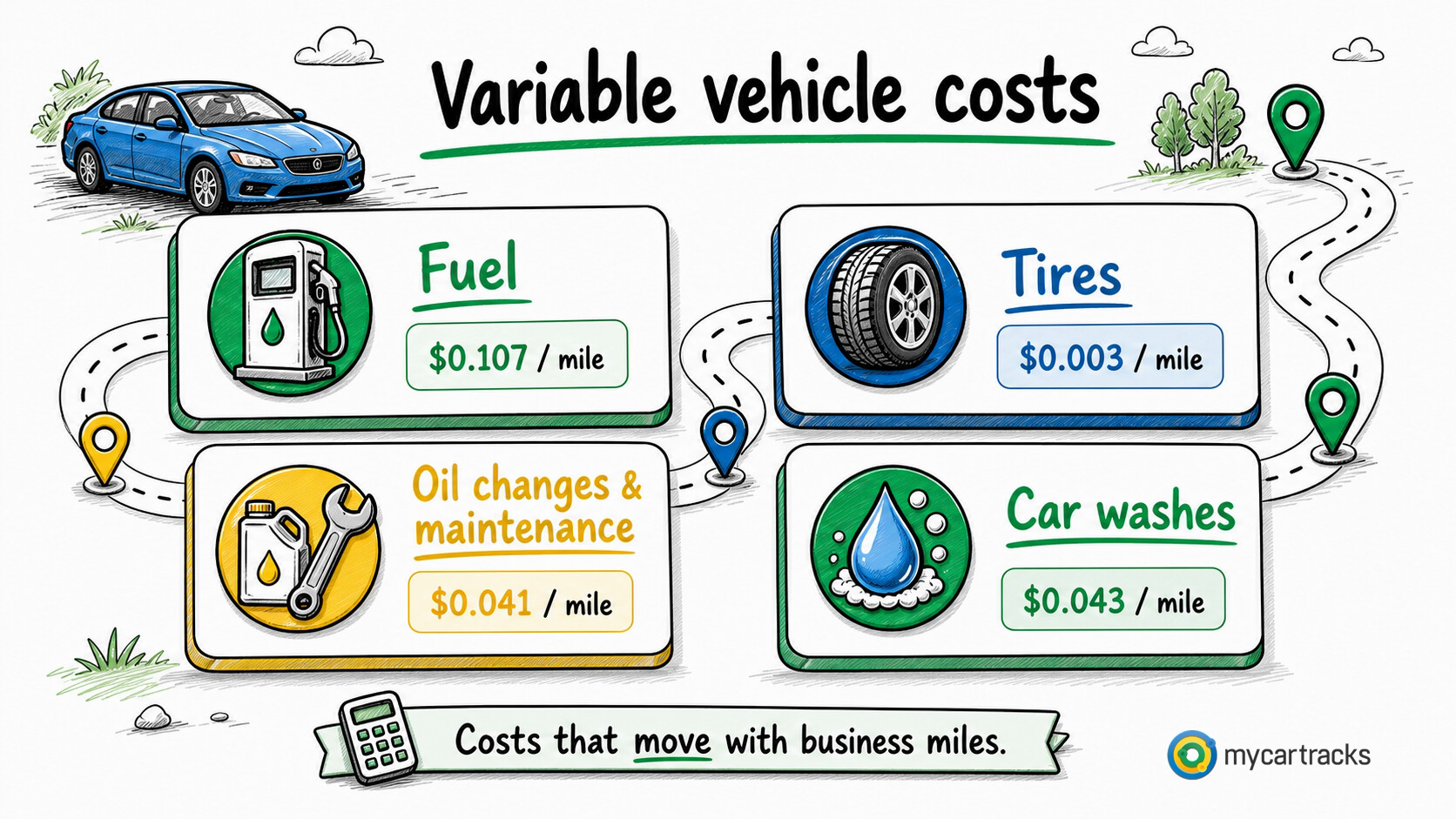

4. Set variable rates

The variable rate reflects the costs that move with driving, such as fuel, tires, oil, and routine maintenance. This is the per-mile part of the plan.

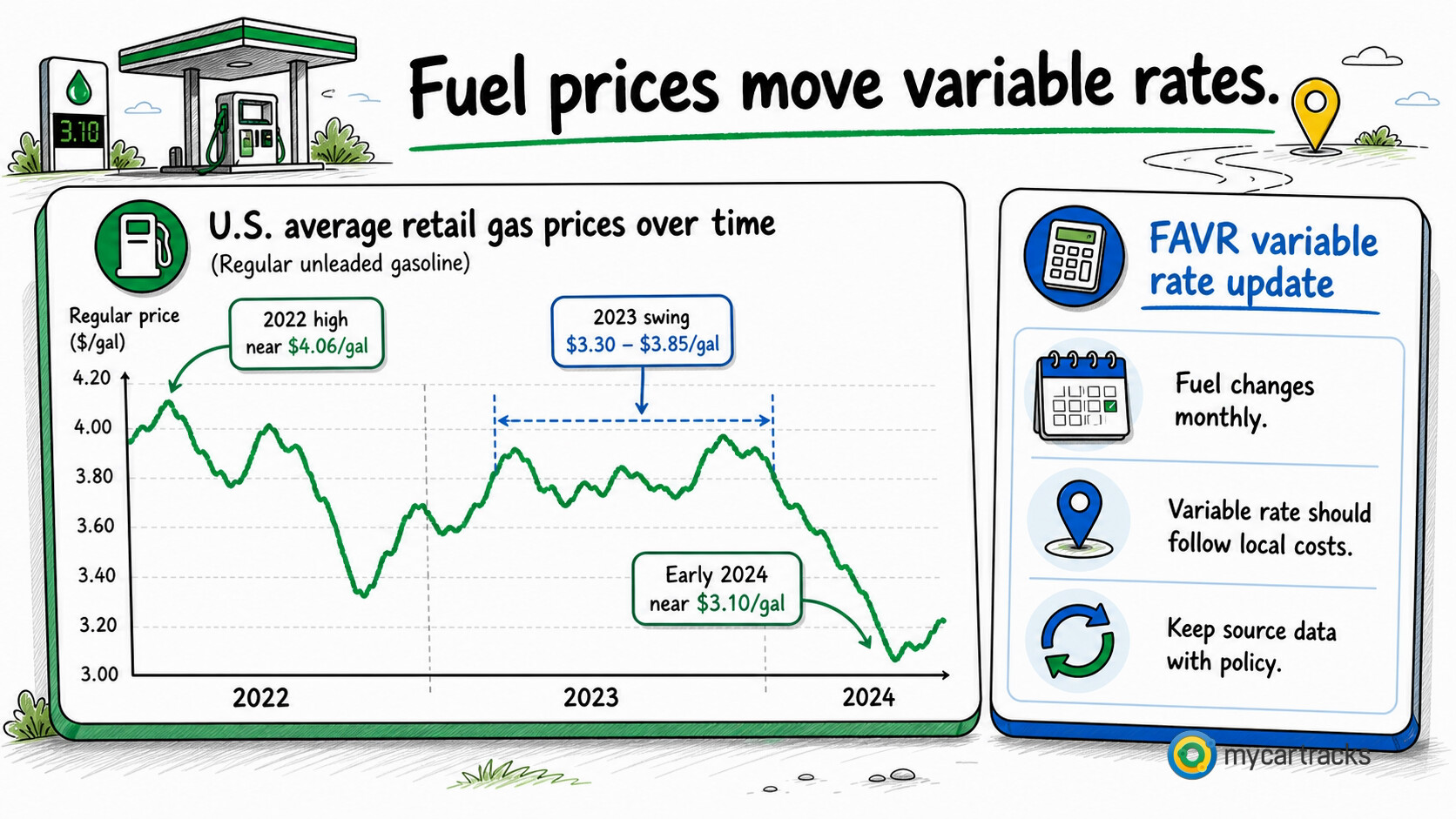

5. Updating variable rates

This is where many companies underestimate the ongoing work. Fuel and other operating costs move, so the variable side cannot be treated as a static number forever.

Many businesses update variable rates monthly or more often.

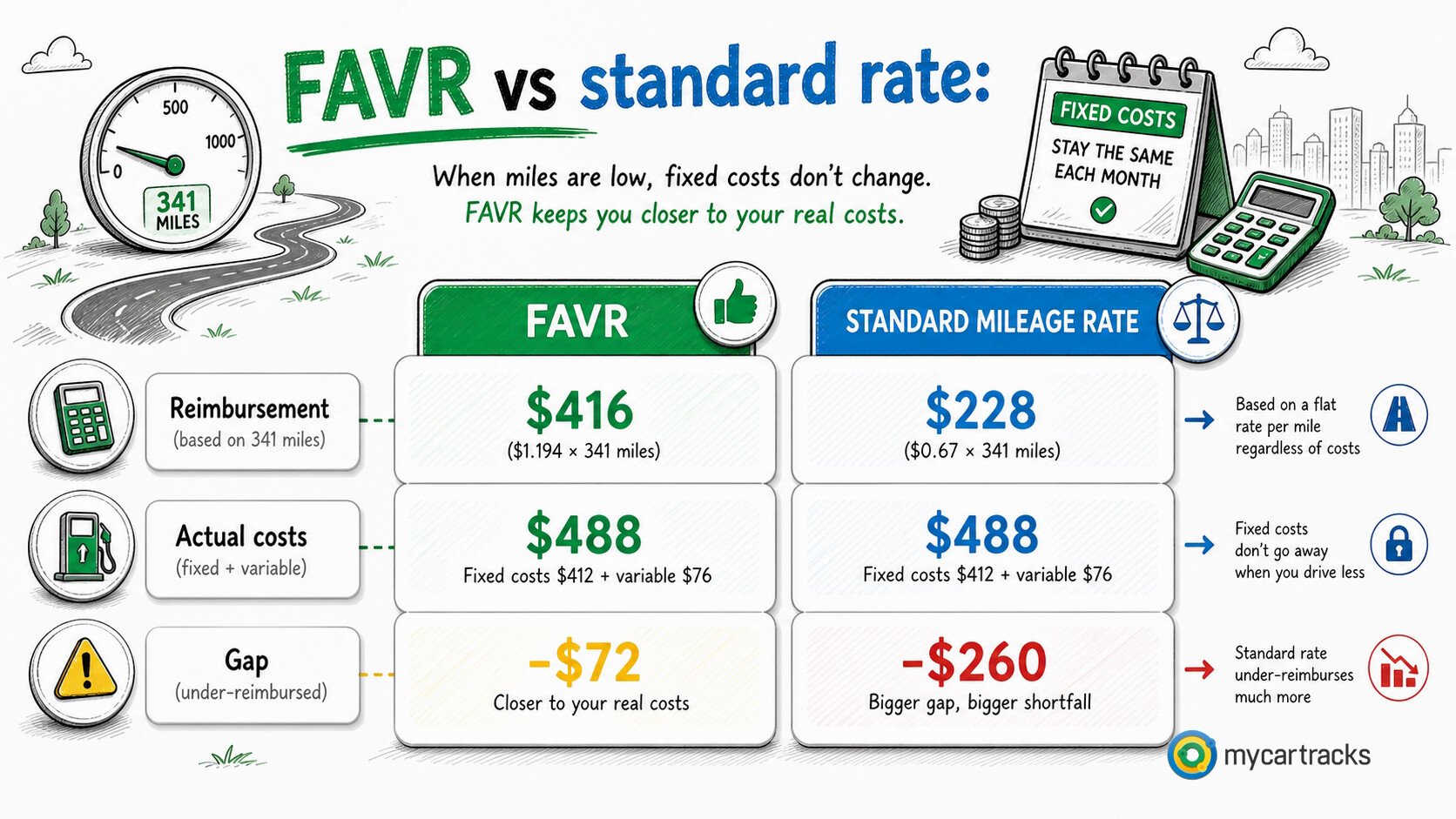

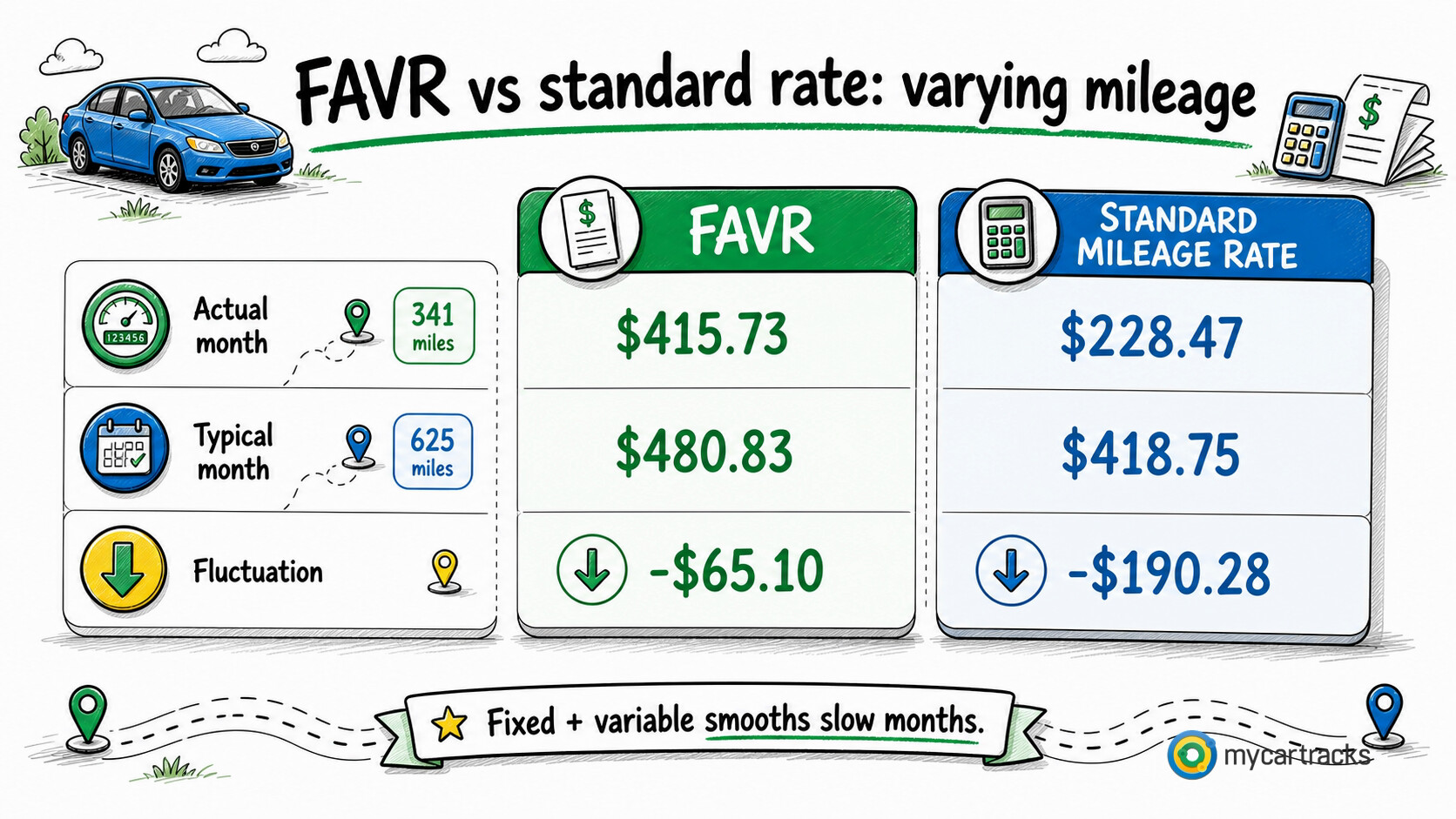

FAVR car allowance examples

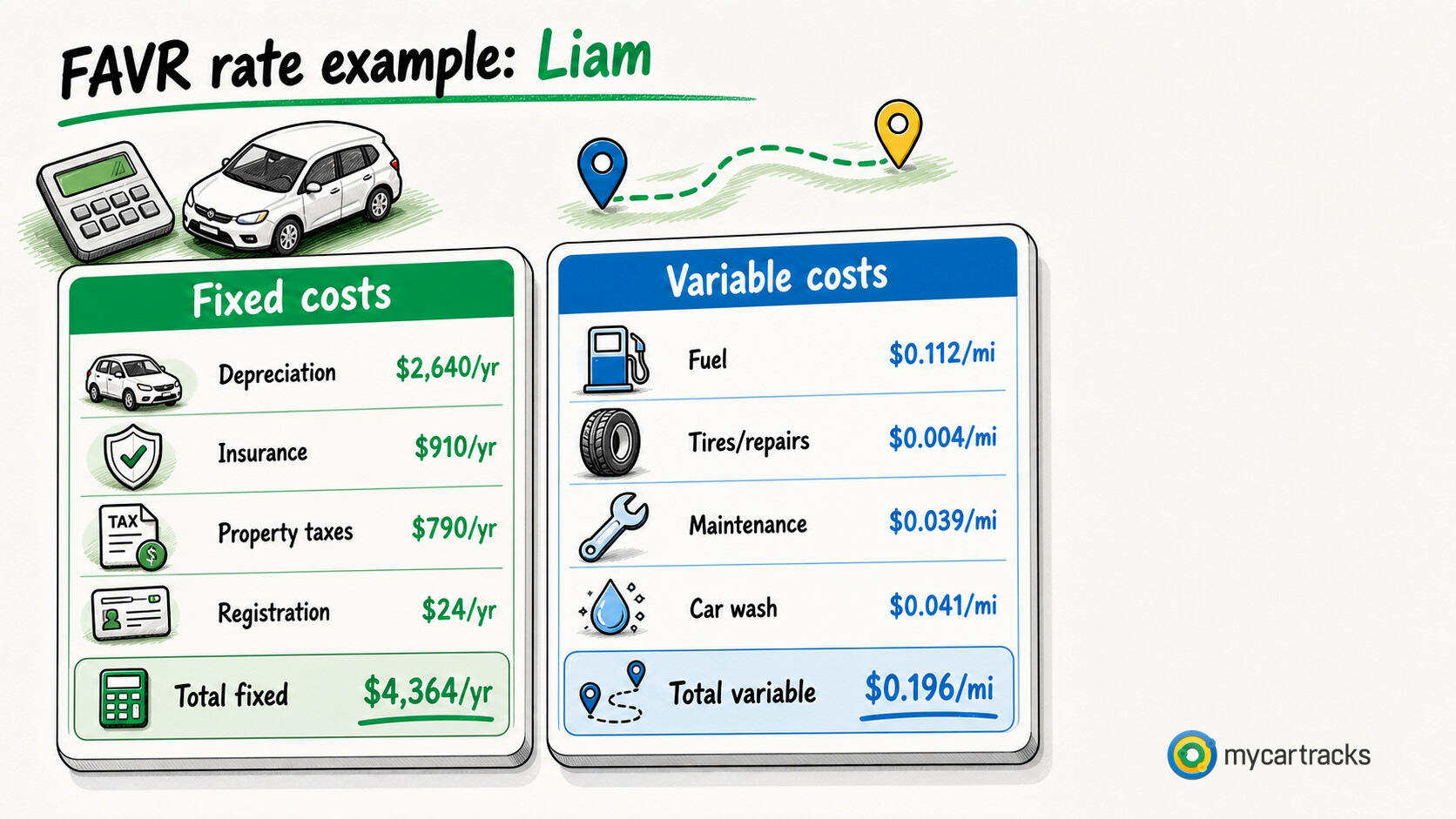

Here is a simple illustration of how the pieces fit together. Imagine Liam has annual fixed costs of $4,364, or about $363.67 per month, and a variable rate of $0.196 per business mile. If Liam drives 625 business miles in a month, the combined reimbursement would be about $486.17.

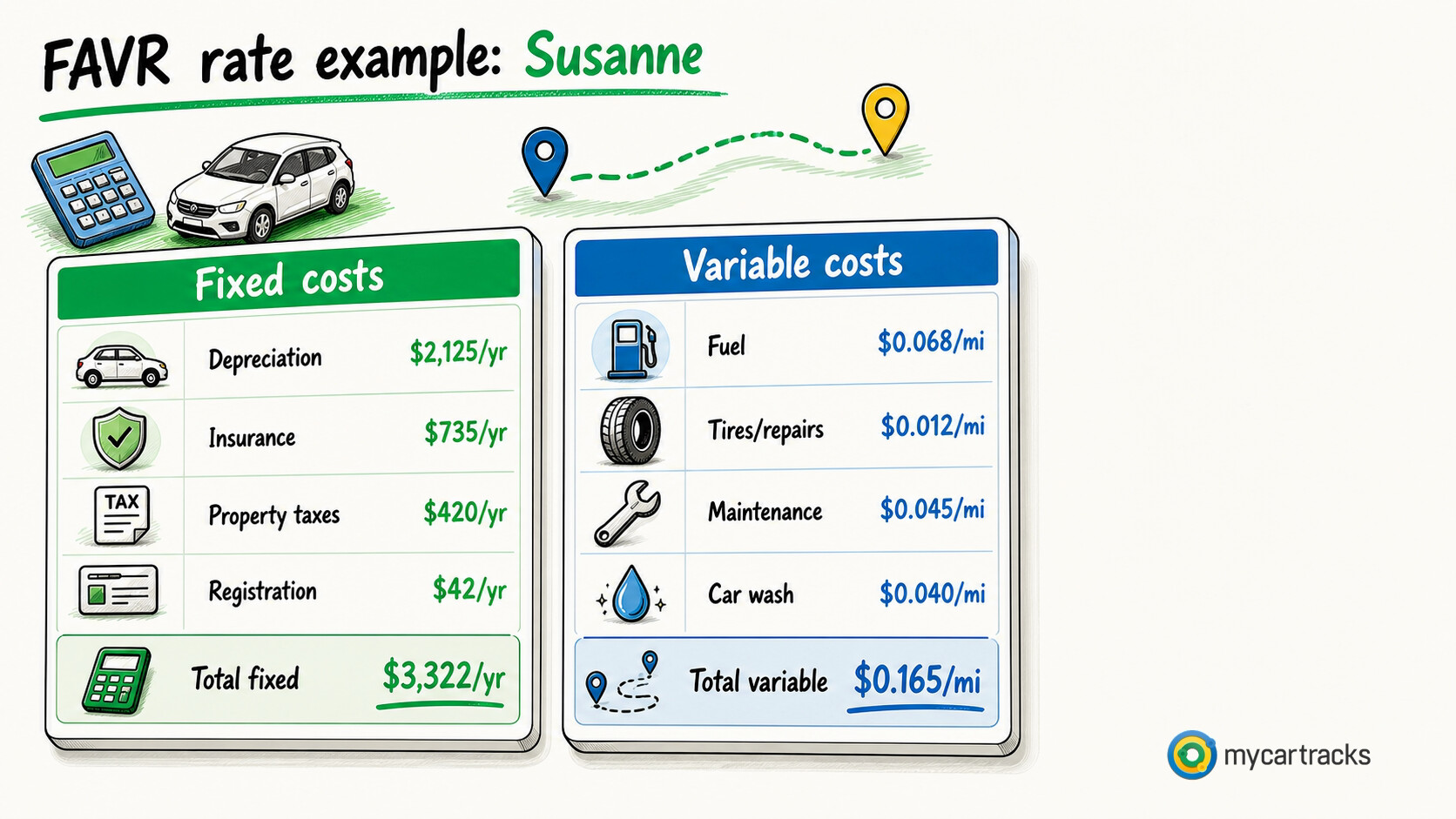

Now imagine Susanne is in a different group with annual fixed costs of $3,322, or about $276.83 per month, and a variable rate of $0.165 per business mile. If Susanne drives 1,250 business miles, the reimbursement would be about $483.08.

Those are only examples, not recommended 2026 rates. The point is that FAVR pays through two levers at once instead of forcing everything through one flat stipend or one national mileage rate.

Payroll and tax review

Payroll review should happen before launch and again whenever the company changes the program. Publication 15 and Revenue Procedure 2019-46 matter together here: the company needs the business connection, the substantiation process, and the excess-payment handling to line up with the way the reimbursement is actually paid.

That is why FAVR should not live in a spreadsheet that payroll never sees. If the company cannot explain the supporting mileage record, the employee eligibility, and the cost assumptions behind the payment, the program is not ready.

Best practices for implementing FAVR reimbursement

The technical rules matter, but most FAVR failures happen in ordinary operational places: weak data, unclear employee communication, stale assumptions, and no defined owner for exceptions.

Establish clear goals for your program

Start by deciding what the program is supposed to accomplish. Are you trying to reduce spend, improve fairness across territories, support a more premium vehicle standard, or make reimbursement more predictable?

Consider self-administering or working with a vendor

Some businesses can run FAVR internally, but they should be honest about the work involved. Someone has to maintain cost assumptions, update variable rates, collect employee certifications, review mileage files, and keep payroll treatment aligned with the plan.

Many businesses use outside support or software for at least part of the process, but the company still needs an internal owner.

Provide robust employee training

Employees need to understand more than “here is your new reimbursement amount.” They need to know what mileage they must submit, what vehicle standards apply, and what happens if their vehicle, role, or territory changes.

Develop a plan for ongoing management and support

Decide who reviews mileage exceptions, who checks annual IRS updates, who collects vehicle and insurance changes, and who handles onboarding for new hires.

A good FAVR program is not just compliant on launch day. It stays documented and current as the business changes.

Getting started

If you are still deciding whether FAVR is worth the effort, compare it against the real alternatives. For some businesses, the better answer is a simpler cents-per-mile program. For others, it is moving away from a taxable allowance. For some high-control roles, it may still be a company-car program or fleet vehicle model.

If you want the recordkeeping layer ready before you make that choice, MyCarTracks automatic mileage tracking can help you capture business mileage consistently. For the broader product view behind trip capture, admin reporting, and exports, use the MyCarTracks homepage and the MyCarTracks features overview.

MyCarTracks workflow

MyCarTracks can help keep the FAVR record stack cleaner:

- Capture trips automatically by employee and vehicle.

- Separate business driving from commuting and personal use.

- Tag reports by territory, role, or reimbursement group.

- Review mileage before the variable-rate calculation is applied.

- Export the claim file with the review period attached.

What to read next

- Car Allowance vs Mileage Reimbursement

- Car Allowance vs Company Car

- Mileage Reimbursement Rules for Employers

- How to Create a Mileage Reimbursement Policy

- Current IRS Mileage Rates for 2026

- IRS Mileage Log Requirements