Mileage tracking and organized travel records can help you deduct qualifying business travel, but only when the trip actually qualifies and the file behind it is strong enough to prove what happened. The current federal rules for travel away from your tax home, temporary assignments, deductible travel costs, and standard meal allowances live in IRS Publication 463 and IRS Topic no. 511, Business travel expenses.

Vehicle miles are only one part of the travel file. Airfare, train fares, taxis, lodging, non-entertainment meals, parking, tolls, and other ordinary and necessary trip costs may also matter, but regular commuting, indefinite assignments, personal side trips, and lavish personal charges do not belong in the same deduction. This article walks through the boundaries before you start filling in Schedule C, Schedule F, or a reimbursement record.

If the hardest part is the mileage-tracking side rather than the tax form, MyCarTracks automatic mileage tracking can help you keep trip records, classifications, and exports ready before filing season turns into reconstruction season.

This article is educational and is not tax, legal, payroll, employment, or financial advice. Mileage rules change by federal tax treatment, state law, employer policy, vehicle program, and tax year. Check the official source and a qualified professional before relying on a calculation.

Quick answer

If a trip is away from your tax home for a real business reason, you may be able to deduct mileage or other transportation costs, lodging, meals subject to the current limits, and related travel expenses. Keep the business purpose, dates, destination, mileage logs, receipts, and any reimbursement records together, and keep commuting, personal extensions, and unsupported extras out of the deduction.

What qualifies as business travel

For this deduction, business travel usually means you leave the general area of your tax home for business and are away long enough that you need sleep or rest to meet the demands of the work. Your tax home is generally your main place of business, not automatically the place where you keep your family home.

A temporary assignment can still qualify, but the rule tightens when the work stops being temporary. If you realistically expect to work in the same location for more than one year, the IRS treats that assignment as indefinite rather than temporary, which usually ends the travel-expense deduction for that location.

The business reason should be clear before you leave. Client meetings, conferences that benefit your trade or business, temporary worksite visits, training tied to your current work, and similar trips can fit. A trip does not become deductible just because you answer a few emails while traveling or meet one client during what is mostly a vacation.

If your real question is whether the drive itself was business mileage or ordinary commuting, read Business Miles vs Commuting Miles before you price anything.

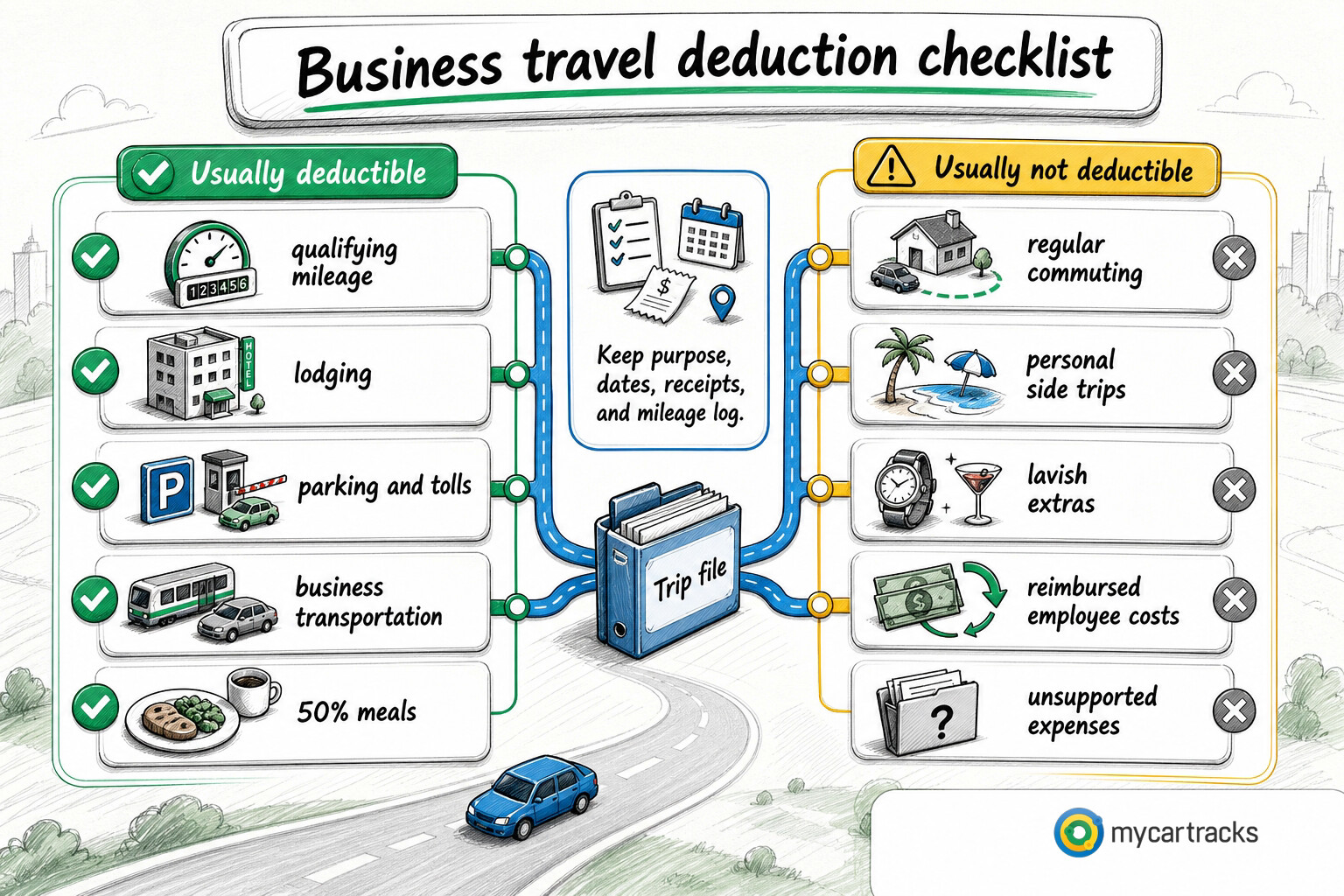

Travel costs that usually qualify

Once the trip qualifies, more than one cost category may belong in the file. Topic no. 511 and Publication 463 both make that broader travel-expense point.

Common deductible categories include:

- airfare, train, bus, or other transportation between your tax home and the business destination

- taxi, rideshare, shuttle, subway, or similar transportation between the airport or station, hotel, and business location

- mileage for using your own vehicle during the trip, or the business-use share of a rental car

- parking fees and tolls tied to the business travel

- lodging

- non-entertainment meals, which are generally limited to 50% of the unreimbursed cost under current federal rules

- laundry, dry cleaning, business calls, baggage shipping, and similar ordinary and necessary trip costs

Employers and some travelers also use standard meal allowances or per diem frameworks where the rules allow it. If you need a current benchmark for travel locations inside the continental United States, the official GSA per diem rates are the source to review alongside the IRS travel rules.

Travel costs that usually do not qualify

The fastest way to break this deduction is to mix a real business trip with costs that belong somewhere else.

These items are common trouble spots:

- regular home-to-work commuting

- costs tied to an indefinite assignment rather than a temporary one

- personal vacation days, family travel, or side trips that do not have a bona fide business purpose

- lavish or extravagant spending that is not reasonable under the circumstances

- entertainment-style expenses that do not qualify as deductible business meals

- personal hotel extras such as movies, gym charges, or similar nonbusiness add-ons

- employee expenses that were already reimbursed, or expenses an employee is trying to claim personally when there is no federal deduction path

Family travel needs special care. If a spouse or child travels with you, their costs are generally personal unless that person is an employee and the travel itself serves a real business purpose.

Mileage tracking and other travel costs

Mileage is one line in the travel file, not the whole file.

If you use your own vehicle during qualifying business travel, you usually choose between the standard mileage method and the actual expense method for the vehicle deduction side. The standard mileage method already bundles core operating costs into the federal per-mile rate, so you generally do not add fuel, maintenance, insurance, or depreciation again under that same method.

Parking and tolls are different. They can still be deductible on top of the mileage calculation when they relate to the business trip. Airfare, train tickets, rideshare charges, lodging, and meals also stay in their own travel-expense lanes rather than being rolled into the mileage number.

That separation matters at filing time. If you need the broader tax-return handoff after sorting the trip record, continue with How to Claim Mileage on Taxes. If you are still deciding how to price the vehicle side, Standard Mileage Rate vs Actual Expenses is the better next step.

Records to keep for business travel

The record should explain the trip to someone who was not there. A pile of receipts without context is weak, and a mileage log without support can be just as weak.

Keep these items together:

- trip dates

- destination and route, including the city or business location involved

- the business purpose for the trip

- who you met, what event you attended, or what job the trip supported

- mileage logs for any vehicle use

- parking, toll, lodging, transportation, and meal receipts where relevant

- calendars, agendas, registration confirmations, work orders, customer emails, or meeting notes that support the business purpose

- reimbursement records if an employer or client already paid part of the cost

- the official rate or rule source used for the year of travel

If you want the vehicle side of that file to stay cleaner from the start, What Is a Mileage Log? and IRS Mileage Log Requirements show what a stronger mileage record looks like.

How to claim the business travel tax deduction

The filing path depends on who incurred the expense and why.

Self-employed filers and sole proprietors

Self-employed workers usually report deductible business travel through Schedule C. Farmers generally use Schedule F. The important point is to classify the trip first, then place each supported cost in the right part of the tax file instead of treating every travel receipt as interchangeable.

Most employees

Most employees are not deducting unreimbursed travel expenses on a personal federal return. In many cases, the real workflow is reimbursement, not deduction. That means the stronger next reads are What Is Mileage Reimbursement?, Mileage Reimbursement Rules for Employees, and How to Create a Mileage Reimbursement Policy.

Limited employee exceptions

Form 2106 still matters for a narrow group of employees, including Armed Forces reservists, qualified performing artists, fee-basis state or local government officials, and employees with impairment-related work expenses. For reservists, Topic no. 511 explains that qualifying overnight travel more than 100 miles from home may allow a deduction limited to the federal per diem and mileage rules plus parking, ferry fees, and tolls.

Ways to protect more of the deduction

The biggest savings usually come from a cleaner process, not from forcing extra receipts into the file.

- Keep business days and personal days separate on mixed-purpose trips.

- Save the rate source for the tax year you are actually filing, not the current year by habit.

- Compare long-drive costs with airfare, train, or rental-car costs before the trip if you still have a real choice.

- Keep parking and tolls outside the mileage line so they do not disappear into the wrong method.

- Use the applicable meal-allowance or per diem framework only when the rules and your role allow it, and keep the location support with the file.

- Review the travel file monthly instead of waiting for year-end.

For self-employed readers who need the bigger deduction workflow around mileage, receipts, and nonvehicle write-offs, Self-Employed Tax Deductions is the deeper support article.

Common mistakes

- treating a work trip as deductible without checking whether it was really away from your tax home

- counting regular commuting as business travel

- folding parking, tolls, meals, and lodging into one vague mileage total

- using the standard mileage rate and then trying to add the same vehicle operating costs again

- keeping receipts without preserving the business purpose

- assuming reimbursed employee travel can always be deducted again on a personal return

- using a current-year rate for an older trip

- waiting until tax season to rebuild the details from memory

If the deduction is challenged

A disallowed business travel deduction does not automatically mean a penalty, but weak records can lead to added tax, interest, and possibly an accuracy-related penalty if the underpayment meets the IRS penalty standards. That penalty is generally 20% of the portion of the underpayment tied to negligence or substantial understatement.

When the IRS questions a travel deduction, the fastest path back to a defensible answer is usually a complete file: trip purpose, dates, destination, mileage log, receipts, and proof of why the travel belonged to the business. If the support is missing, you may need to remove the unsupported amount or correct the return.

Practical example

Suppose a self-employed consultant flies to another city for a two-day client workshop, uses a rideshare from the airport to the hotel, pays for lodging, buys meals during the trip, and drives a personal vehicle to the airport and back. The file should keep those costs in separate lanes: airfare, local transportation, lodging, meals subject to the current limit, airport parking, and the qualifying vehicle mileage.

Now add one extra vacation day after the workshop. That personal extension does not belong in the same deduction by default just because the business trip happened first. The cleaner record shows which days and costs were business-related, which were personal, and which official rule source was used for the filing year.

MyCarTracks workflow

Use MyCarTracks as the trip-record layer first, then let the tax file follow the facts.

- Capture vehicle trips while the details are still fresh.

- Classify business, commuting, and personal driving before the route becomes a guess.

- Export mileage records by vehicle and tax year, then attach receipts and purpose notes for the rest of the travel file.

- Keep the mileage report with the travel receipts, reimbursement notes, and official source pages used for the filing decision.

For the broader product view behind trip capture, reporting, and exports, see MyCarTracks and the reporting tools on the MyCarTracks features page.

What to read next

- Business Miles vs Commuting Miles

- Standard Mileage Rate vs Actual Expenses

- How to Claim Mileage on Taxes

- What Is a Mileage Log?